📘 Profit as a Function of Quantity Sold

1️⃣ Basic Definition of Profit

By definition:

Profit = Revenue – Cost

This means:

👉 A company makes profit when the money it earns is greater than the money it spends.

2️⃣ What is Revenue?

Revenue = Price × Quantity

Where:

-

P = price per unit

-

Q = number of units sold

So if you sell more units, revenue increases.

3️⃣ What is Cost?

Cost has two parts:

🔹 Fixed Costs

These do NOT change with production.

Examples:

-

Rent

-

Salaries

-

Insurance

-

Depreciation

Even if the company produces zero units, fixed costs still exist.

🔹 Variable Costs

These change depending on production.

Examples:

-

Raw materials

-

Packaging

-

Sales commissions

-

Electricity for machines

The more you produce, the higher the variable cost.

So total cost is:

Cost = Fixed Cost + (Variable Cost × Q)

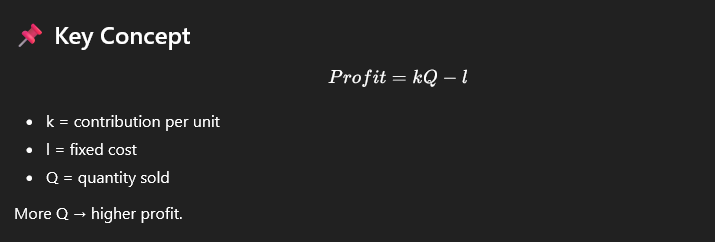

4️⃣ Combining Everything

We substitute Revenue and Cost into the Profit formula:

This means:

👉 Profit depends on how many units you sell (Q).

It is a linear function.

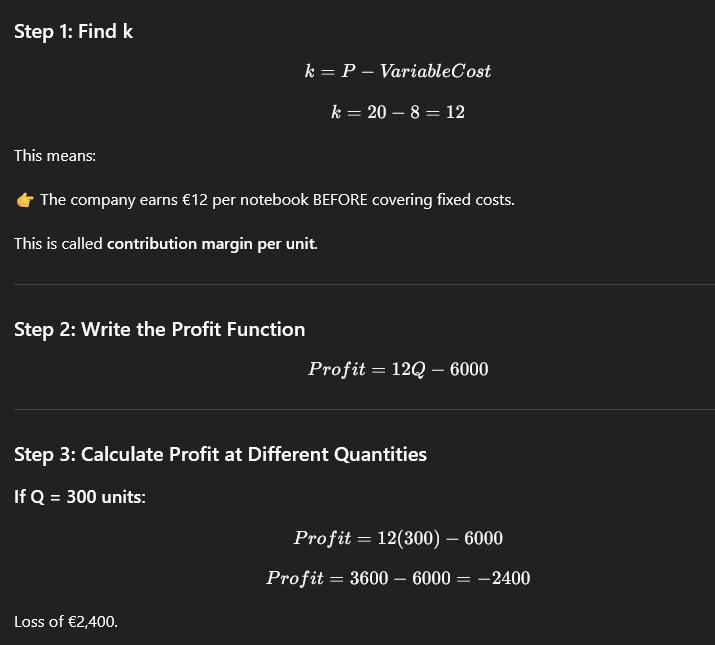

📊 Example

Let’s imagine a company that sells notebooks.

Given:

-

Price per notebook (P) = €20

-

Variable cost per notebook = €8

-

Fixed costs = €6,000

🎯 What You Should Understand

-

Profit depends on quantity sold.

-

There is a break-even quantity.

-

Fixed costs create the initial loss.

-

After break-even, profit increases linearly.

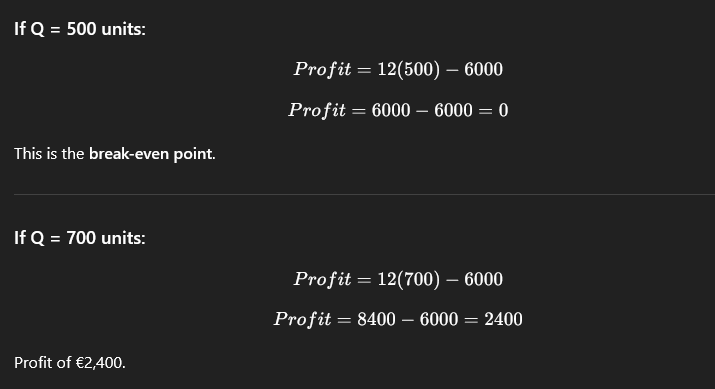

Given:

-

Price (P) = €20

-

Variable Cost per unit = €8

-

Fixed Cost = €6,000

-

Contribution per unit (k) = 20 − 8 = €12

Profit function:

Profit=12Q−6000

📊 Profit Table for Different Quantities

| Quantity Sold (Q) | Revenue (20×Q) | Variable Cost (8×Q) | Total Cost | Profit (12Q − 6000) |

|---|---|---|---|---|

| 0 | €0 | €0 | €6,000 | -€6,000 |

| 200 | €4,000 | €1,600 | €7,600 | -€3,600 |

| 300 | €6,000 | €2,400 | €8,400 | -€2,400 |

| 400 | €8,000 | €3,200 | €9,200 | -€1,200 |

| 500 | €10,000 | €4,000 | €10,000 | €0 (Break-even) |

| 600 | €12,000 | €4,800 | €10,800 | €1,200 |

| 700 | €14,000 | €5,600 | €11,600 | €2,400 |

| 800 | €16,000 | €6,400 | €12,400 | €3,600 |

| 1,000 | €20,000 | €8,000 | €14,000 | €6,000 |

🎯 What You Can Observe

-

At Q = 0 → Loss equals fixed cost.

-

At Q = 500 → Profit = 0 (Break-even point).

-

After 500 units → Profit increases by €12 per additional unit.

-

Profit increases linearly.

Comments are closed.